How to Calculate Accounts Receivable Turnover

Learn how to calculate accounts receivable turnover, understand the formula, and improve collections to strengthen cash flow and financial stability.

- Last Updated: Jun 26, 2026

-

Dadhich Rami

Dadhich Rami

Learn how to calculate accounts receivable turnover, understand the formula, and improve collections to strengthen cash flow and financial stability.

Dadhich Rami

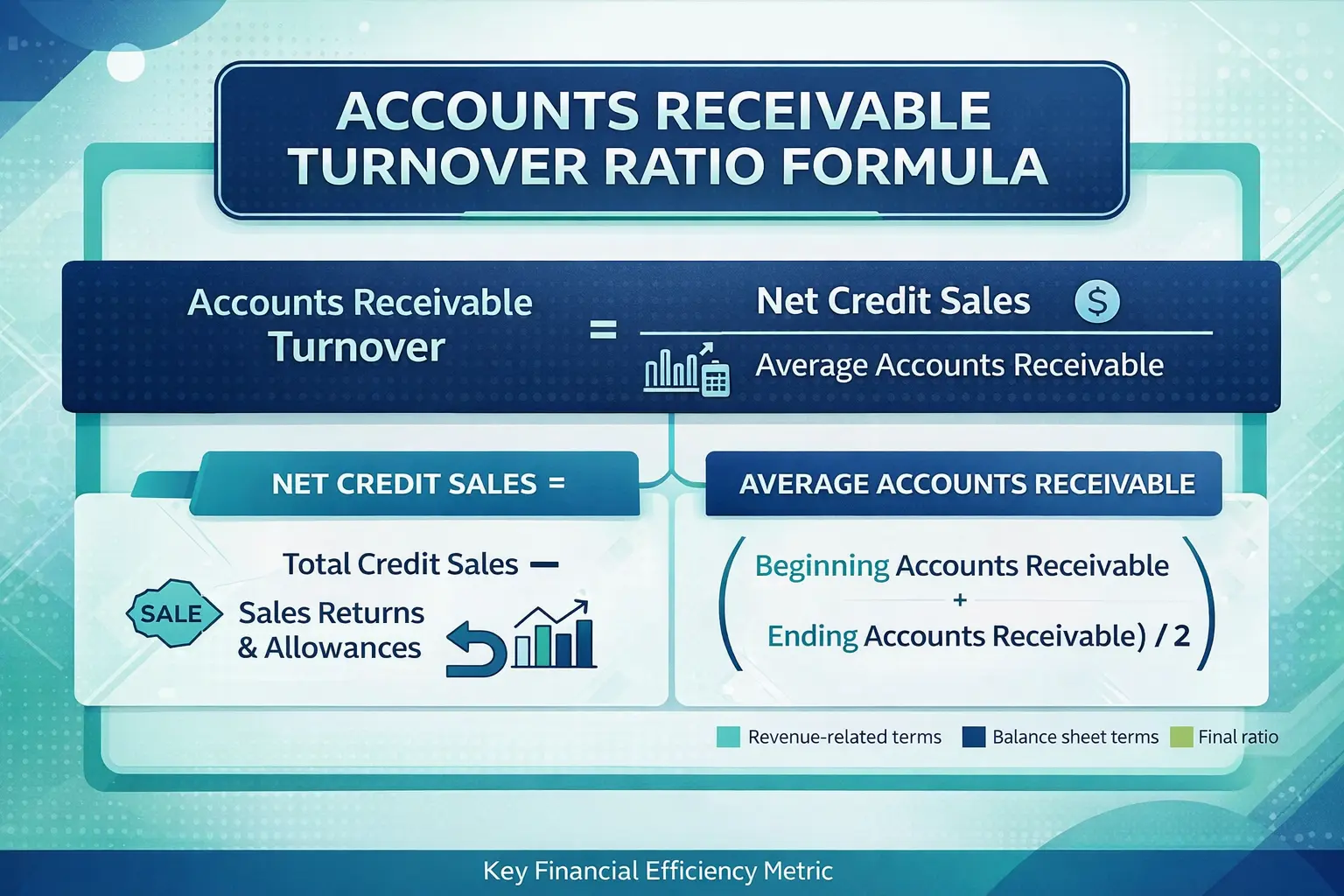

You calculate accounts receivable turnover by dividing net credit sales by average accounts receivable, where average AR equals (beginning AR plus ending AR) divided by 2. For example, $500,000 in net credit sales divided by $100,000 in average receivables gives a turnover ratio of 5, meaning the business collects its receivables five times a year. Dividing 365 by that ratio converts it into a collection period, so a turnover of 5 equals roughly 73 days to get paid. A higher ratio signals faster collections, stronger cash flow, and lower bad debt risk, which is why teams track it alongside DSO and lean on AR automation to improve it.

The Accounts Receivable Turnover ratio measures how efficiently a business collects payments from its customers. It shows how many times receivables are converted into cash during a given period.

This metric is widely used to evaluate collection efficiency and overall cash flow performance.

Accounts Receivable Turnover = Net Credit Sales ÷ Average Accounts Receivable

Average Accounts Receivable is calculated as: (Beginning AR + Ending AR) ÷ 2

This helps smooth out variations and gives a more balanced measure for the turnover calculation.

Start by identifying the total sales made on credit during the period you are analyzing. This information is usually available in the company’s income statement or sales records. Make sure to exclude any cash sales, as they do not form part of receivables. If there are returns or discounts, subtract them to arrive at the net credit sales figure.

Next, determine the accounts receivable balances at the beginning and end of the period. These figures are typically found on the balance sheet. Add both values and divide by two to calculate the average. This step is important because receivables can change throughout the period, and using an average gives a more accurate representation of outstanding balances.

Average Accounts Receivable = (Beginning AR + Ending AR) ÷ 2

Once you have both net credit sales and average accounts receivable, divide the net credit sales by the average receivables. The result is your accounts receivable turnover ratio, which indicates how many times receivables are collected during the period.

Accounts Receivable Turnover = Net Credit Sales ÷ Average AR

To understand how accounts receivable turnover is calculated in a real-world scenario, consider the following example of a company analyzing its performance over a one-year period:

These figures represent the total credit sales made during the year and the outstanding receivables at the start and end of the period.

Since receivables can change throughout the year as customers make payments and new credit sales are added, it’s important to calculate the average balance instead of relying on a single figure.

(80,000 + 120,000) ÷ 2 = 100,000

This means that, on average, the business had $100,000 tied up in unpaid customer invoices during the year.

Next, divide the net credit sales by the average accounts receivable:

500,000 ÷ 100,000 = 5

This gives an accounts receivable turnover ratio of 5 times.

A turnover ratio of 5 means that the company collected its average receivables five times during the year. In practical terms, this indicates how frequently outstanding invoices are converted into cash within the given period.

To break this down further, the company is cycling through its receivables roughly every few months, showing a consistent pattern of collections.

This result can also be used to estimate how long it takes to collect payments:

Collection Period = 365 ÷ 5 = 73 days

This means that, on average, it takes the business about 73 days to collect payments from customers.

A turnover ratio of 5 generally suggests moderate collection efficiency. If the company’s credit terms are around 60 days, a 73-day collection period may indicate slight delays in payments.

A higher turnover ratio would mean faster collections and improved cash flow, while a lower ratio could signal inefficiencies in the collection process or issues with customer payments.

To determine how long it takes to collect payments:

Collection Period = 365 ÷ Accounts Receivable Turnover

Using the example:

365 ÷ 5 = 73 days

This indicates the average time required to collect outstanding receivables.

This metric is often analyzed alongside Days Sales Outstanding (DSO) to get a clearer picture of collection timelines and efficiency.

If your turnover ratio is low, focus on:

Managing accounts receivable manually can lead to delays, missed follow-ups, and inconsistencies in tracking outstanding invoices. As transaction volumes grow, these inefficiencies can directly impact how quickly a business is able to convert receivables into cash.

Using AR automation software helps organize the entire process by centralizing invoice tracking, automating payment reminders, and reducing manual intervention. This provides collection efficiency and better visibility into receivables, allowing businesses to take timely action and maintain a healthy cash flow.

The accounts receivable turnover ratio is a key indicator of how efficiently a business converts credit sales into cash. By applying the correct formula, companies can evaluate the effectiveness of their credit policies and collection processes with clarity.

Tracking this ratio over time provides valuable insights into payment patterns, helping identify delays, inefficiencies, or risks in collections. With consistent monitoring and the right improvements, businesses can strengthen cash flow, reduce outstanding receivables, and maintain better financial stability.

The data required for this calculation is usually found in financial statements. Net credit sales can be taken from the income statement or sales records, while beginning and ending accounts receivable are available on the balance sheet.

40%

DSO reduction70%

less manual work95%

cash match accuracyFind out exactly how much time and money your AR team can save with Quick Receivable. No commitment, no setup required.

Managing 175,000 invoices per month in production